By Samir El Khoury

The most important events of the past week

United States of America

· The building permits index recorded 1.489 million, surpassing expectations (1.470M) but lower than the previous reading (1.493M).

· The new home sales index recorded 661K, which is lower than expectations (680K) but higher than the previous reading (651K).

· The core durable goods orders index declined on a monthly basis, recording a contraction of 0.3%, which is lower than expectations (0.2%) and the previous reading (-0.1%).

· The Consumer Confidence Index declined, recording 106.7 points, which is lower than expectations (114.8) and the previous reading (110.9).

· The GDP index declined, recording 3.2%, which is lower than expectations (3.3%) and the previous reading (4.9%).

· US crude oil inventories rose by 4.20 million barrels, which exceeded expectations (3.10M) and the previous reading (3.51M).

· The core personal consumption expenditures price index recorded 2.8% on an annual basis, which is in line with expectations, but lower than the previous reading (2.9%).

· The initial jobless claims index rose to 215K, which exceeded expectations (209K) and the previous reading (202K).

· The pending home sales index declined, recording a contraction of 4.9%, which is lower than expectations (1.4%) and the previous reading (5.7%).

· The Manufacturing Purchasing Managers’ Index rose, recording a growth of 52.2 points, which exceeded expectations (51.5) and the previous reading (50.7).

· The construction spending index declined on a monthly basis, recording a contraction of 0.2%, which is a lower percentage than expectations (0.2%) and the previous reading (1.1%).

· The Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index fell to 47.8 points, which is lower than expectations (49.5) and the previous reading (49.1).

· The Michigan Consumer Confidence Index declined, recording 76.9 points, which is lower than expectations (79.6) and the previous reading (79.2).

Eurozone

· The headline consumer price index recorded on an annual basis 2.6%, which was higher than expectations (2.5%) but lower than the previous reading (2.8%). The core consumer price index (which excludes food and energy) recorded on an annual basis 3.1%, which was higher than expectations (2.9%) but lower than the previous reading (3.3%).

· The Manufacturing Purchasing Managers’ Index recorded a contraction of 46.5 points, which was higher than expectations (46.1) but lower than the previous reading (46.6).

United Kingdom

· The Manufacturing Purchasing Managers’ Index rose, recording a contraction of 47.5 points, a percentage that exceeded expectations (47.1) and the previous reading (47.0).

Australia

· The Manufacturing Purchasing Managers’ Index recorded a contraction of 47.8 points, which is higher than (47.7) but lower than the previous reading (50.1).

· The retail sales index recorded on a monthly basis 1.1%, which is lower than expectations (1.6%) and the previous reading (-2.1%).

New Zealand

· The Central Bank of New Zealand decided to keep interest rates unchanged, with the key interest rate remaining at 5.50%, in line with market expectations.

China

· The non-manufacturing purchasing managers index rose, registering a growth of 51.4 points, which exceeded expectations (50.9) and the previous reading (50.7).

· The Manufacturing Purchasing Managers’ Index recorded a contraction of 49.1 points, which is in line with expectations but lower than the previous reading (49.2).

· The Caixin Manufacturing Purchasing Managers’ Index (PMI) rose by 50.9 points, which exceeded expectations (50.7) and the previous reading (50.8).

Japan

· The Consumer Price Index recorded an annual rate of 2.0%, which exceeded expectations (1.9%) but was lower than the previous reading (2.3%).

· The industrial production index declined on a monthly basis, recording a contraction of 7.5%, which is lower than expectations (-6.7%) and the previous reading (1.4%).

· The retail sales index recorded on an annual basis 2.3%, which was higher than expectations (2.0%) but lower than the previous reading (2.4%).

The most important events of this week

This week, financial markets are eagerly awaiting the release of several key economic indicators:

· The Building Permits Index in Australia and the Consumer Price Index in Switzerland are released today.

· On Tuesday, the markets are awaiting the services PMI in Australia, Japan, the Eurozone, Britain, and the United States of America, the consumer price index in Tokyo, Japan, the services PMI from Caixin in China, and the factory orders and non-manufacturing purchasing managers indexes issued by the Institute for Supply Management (ISM) in the United States of America.

· On Wednesday, markets eagerly anticipate the interest rate decision from the Central Bank of Canada, with expectations leaning towards maintaining rates at 5.00%. Additionally, investors are awaiting the testimony of US Federal Reserve Chairman Jerome Powell. Economic indicators scheduled for release include GDP and retail sales figures in Australia, the construction PMI in Britain, retail sales data in the Eurozone, the Ivey Purchasing Managers’ Index in Canada, the ADP non-farm private sector jobs report, job opportunities data, and US crude oil inventories.

· As for Thursday, markets are poised for the interest rate decision from the European Central Bank, with expectations leaning towards maintaining rates at 4.50%. Attention is focused on the speech and tone of European Central Bank President Christine Lagarde regarding the future interest rate trajectory. Investors are also anticipating the testimony of US Federal Reserve Chairman Jerome Powell. Scheduled economic indicators include exports, imports, and foreign exchange reserves in China, the unemployment rate in Switzerland, initial jobless claims in the United States, and building permits in Canada.

· Finally, on Friday, the Eurozone’s gross domestic product, non-farm payrolls report, the unemployment rate, and average hourly wages indicators in the United States of America will be released, in addition to the rates of change in employment and unemployment in Canada.

Technical Analysis:

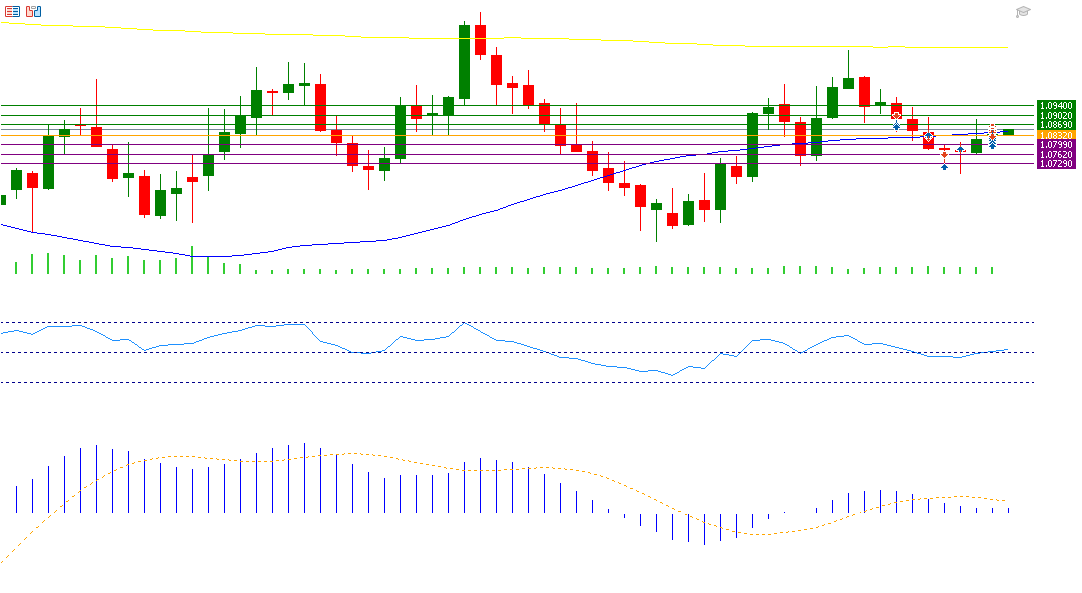

EUR/USD:

If the euro against the dollar breaks the pivot point of 1.0832, it may potentially target and test the support levels of 1.0799, 1.0762, and 1.0729. Conversely, if it surpasses the pivot point, it is likely to test resistance levels of 1.0869, 1.0902, and 1.0940.

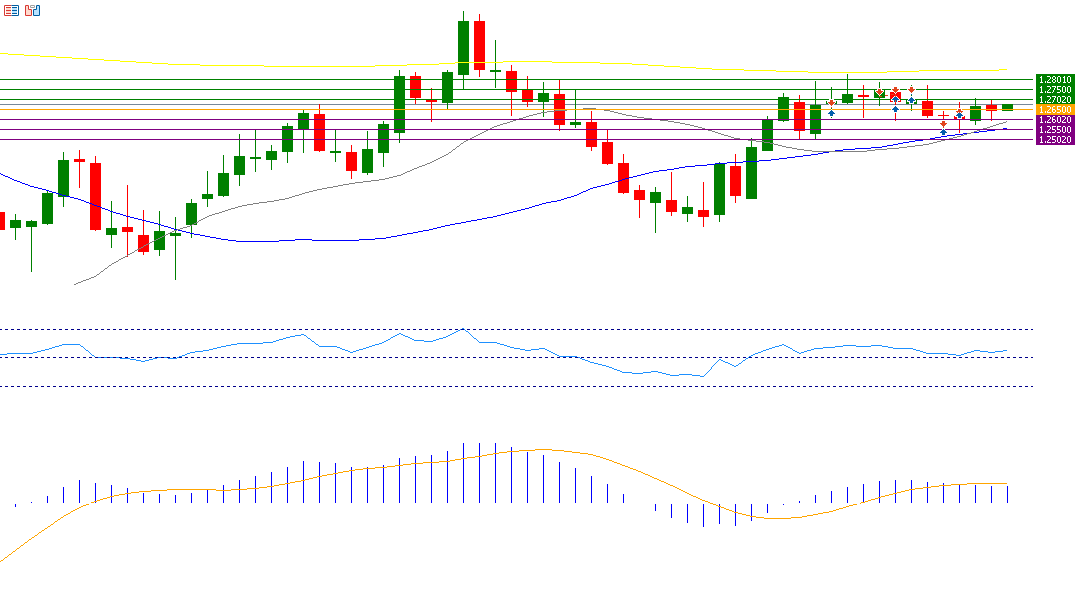

GBP/USD:

If the pound against the dollar breaks the pivot point of 1.2650, it has the potential to test the support levels of 1.2602, 1.2550, and 1.2502. However, if it exceeds the pivot point, it may test resistance levels of 1.2702, 1.2750, and 1.2801.

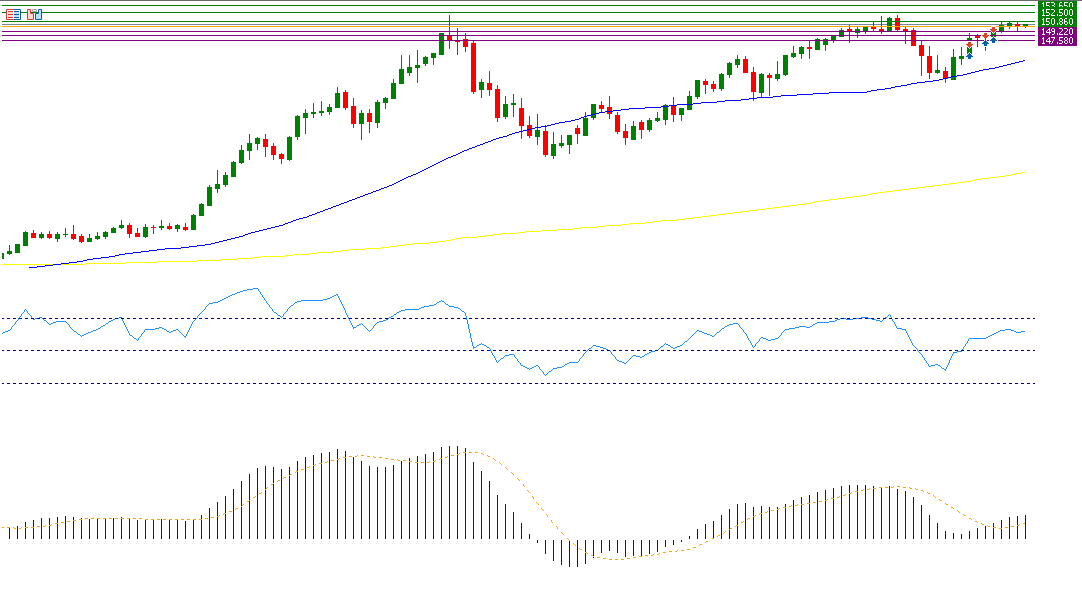

USD/JPY:

If the pivot point of 150.03 is broken for the dollar against the yen, there is a possibility that it will target the support levels 149.22, 148.39, and 147.58. But if it exceeds the pivot point, it is likely to target the resistance levels 150.86, 151.67, and 152.50.

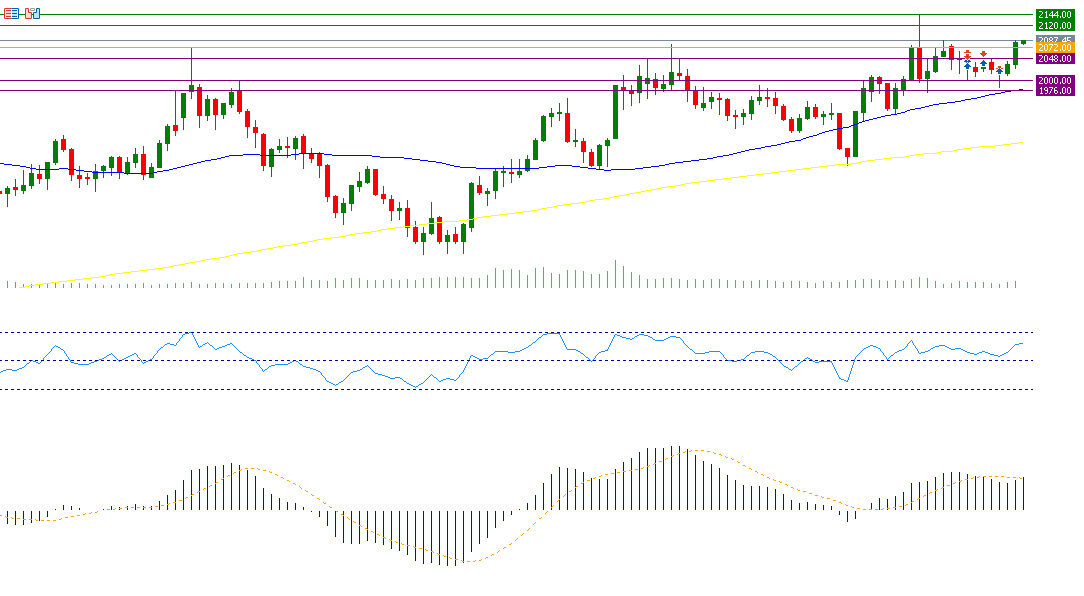

GOLD:

If the pivot point of 2072 is broken for gold, there is a possibility that it will target the support levels 2048, 2000, and 1976. But if it exceeds the pivot point, it is likely to target the resistance levels 2120, 2144, and 2192.

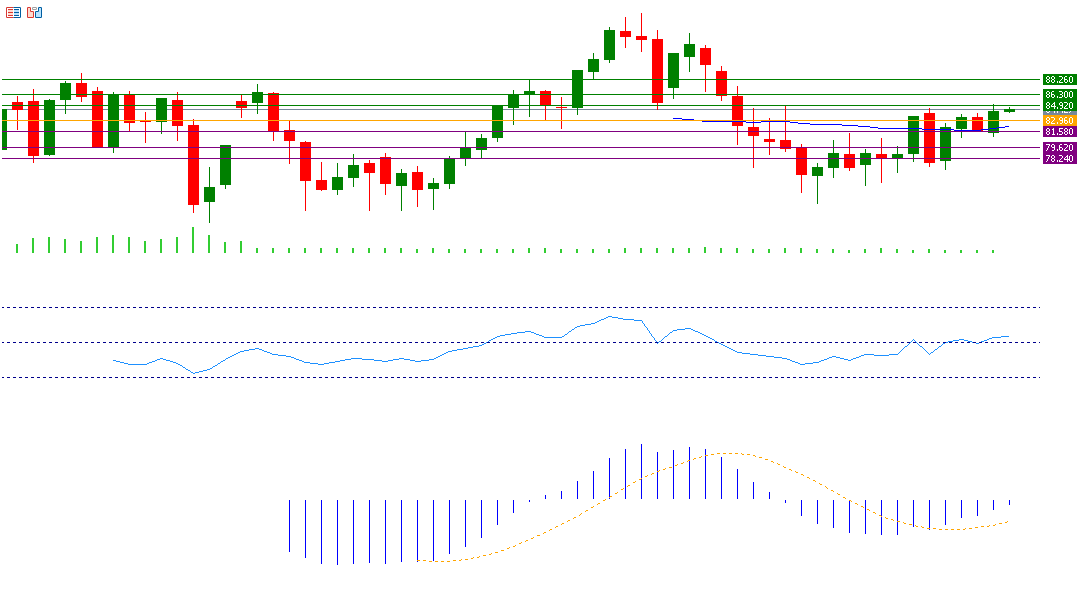

BRENT CRUDE OIL:

If the pivot point of 82.96 for crude oil is broken, there is a possibility that it will target the support levels of 81.58, 79.62 and 78.24. If it exceeds the pivot point, it is likely to target the resistance levels 84.92, 86.30, and 88.26.

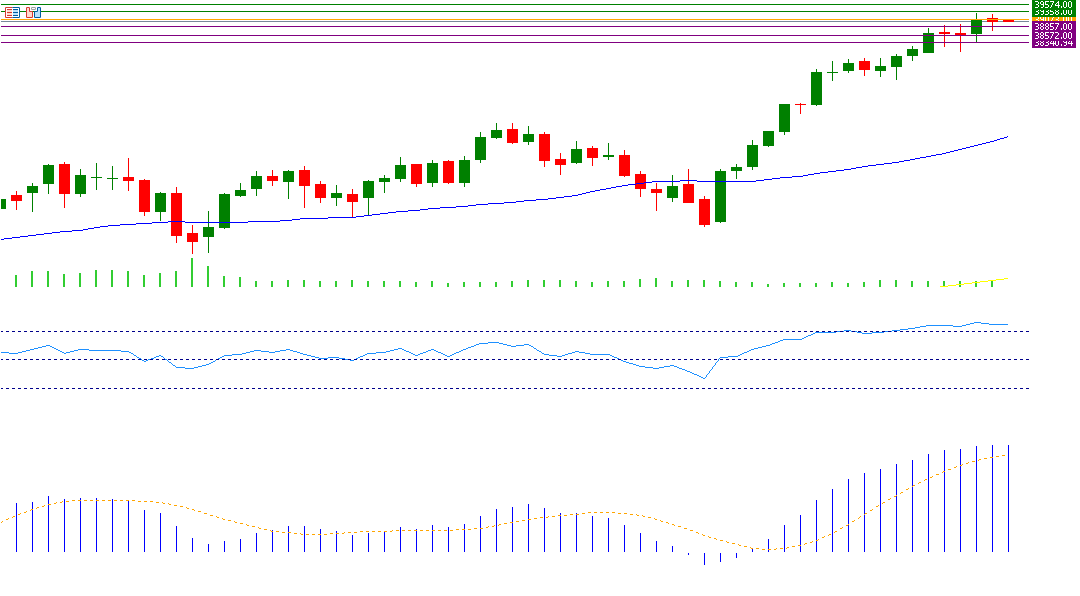

US30:

If the pivot point of 39,073 for the Dow is broken, there is a possibility that it will target the support levels 38,857, 38,572 and 38,356. If it exceeds the pivot point, it is likely to target the resistance levels 39,358, 39,574, and 39,859.

Please note that this analysis is provided for informational purposes only and should not be considered as investment advice.

Taurex is the trading name of Zenfinex Global Limited, Stochastic Africa SL Ltd, Zenfinex Global LLC, and Zenfinex Limited.

Zenfinex Global Limited is registered in the Republic of Seychelles with registration number: 8428731-1 and is regulated by the Financial Services Authority of Seychelles (license number SD092). Its registered office address is F20, 1st Floor, Eden Plaza, Eden Island, Seychelles.

Stochastic Africa (SL) Limited is a company registered in Sierra Leone with Company Number: SL270319STOCH05271 and is licensed by the Bank of Sierra Leone under license number BSL/SAL/2023 and with the registered office at 148D Wilkinson Road, Freetown, Sierra Leone.

Zenfinex Global LLC is a company registered with the Financial Services Authority in Saint Vincent and the Grenadines under registered number 138 LLC 2019. Its registered office is Hinds Building, Kingstown, Saint Vincent, and the Grenadines.

Zenfinex Limited is a company registered in England and Wales under registered number: 11077380. Authorised and regulated by the Financial Conduct Authority under firm reference number 816055. Its registered office is 4th Floor, 4 Eastcheap, London, EC3M 1AE, United Kingdom.

*All trading involves risk